Uptime Institute

Uptime InstituteEnterprise IT and the public cloud: What the numbers tell us

The spectacular growth of the public cloud has many drivers, only one of which is the deployment, redevelopment or migration of enterprise IT into the cloud. But many groups within the industry — data center builders and operators, hardware and software suppliers, networking companies, and providers of skills and services alike — are closely watching the rate at which enterprise workloads are moving to the cloud, and for good reason: Enterprise IT is a proven, high-margin source of revenue, supported by large, reliable budgets. Attracting — or keeping — enterprise IT business is critical to the existing IT ecosystem.

The popular view is that enterprise IT is steadily migrating to the public cloud, with the infrastructure layers being outsourced to cheaper, more reliable, more flexible, pay-as-you-go cloud services. Amazon Web Services (AWS), Microsoft Azure and Google are the biggest beneficiaries of this shift. There is very little contention on this directional statement.

It is only when we add the element of TIMEFRAME that we start to lose universal agreement. It is frequently reported and forecasted that we will reach a tipping point where traditional data center centric style approaches (including non-public cloud or non-SaaS provided IT) will become prohibitively expensive, less efficient and too difficult to support. Looking at any complex system of change, its pretty clear this is sound thinking, BUT when will this happen? Some of the data published by industry analysts and (self-)proclaimed experts suggests it will be many years, while other studies suggest we will soon be nearing that point. Its really a mixed bag depending on who you are talking to.

The Uptime Intelligence view is this kind of genetic fundamental change usually happens much more slowly than the technologists predict and we expect the traditional infrastructure platforms (including in-house data centers and customer managed co-location sites) to be the bedrock of Enterprise IT for many years to come.

So how can the views vary so widely? In 2018, 451 Research’s “Voice of the Enterprise Digital Pulse” survey asked 1,000 operators, “Where are the majority of your workloads/applications deployed — now, and in two years’ time?” In the second half of 2018, 60% said the bulk of their loads were “on-premises IT”. Only 20% said the bulk of their workloads were already in the public cloud or in SaaS.

That is still a fair portion in the public cloud or SaaS, but it has taken time: public cloud has been available for about 13 years (AWS debuted in 2006) and SaaS, over 20 (Salesforce was launched in 1999). Over this period, enterprises have had the choice of co-location, managed hosting (cloud or otherwise), or cloud and SaaS. If we view all but traditional IT infrastructure as “new,” a rough summary might be to say that, over that time, just over a third of enterprises have mostly favored the public cloud as a location for their NEW applications, while two-thirds of organizations have favored other ways of running their IT that give them more control.

But what happens next? 451 Research’s data (see below) does suggest that the move away from on-site, traditional IT is really starting to step up. Thirty-nine percent (39%) of organizations say that by 2020, the bulk of their data will be in SaaS or a public cloud service. That’s a big number, although it is an aspiration — many organizations have not transitioned anywhere near as fast as they would have liked. But look at this another way: Even in 2020, nearly half of all organizations say their loads will still mostly be in enterprise data centers or under their control in a co-location facility. So a lot of enterprise infrastructure will remain in place, with over a third of these organizations still hosting applications mostly in their own data centers.

But the real story is buried in the science of survey design… the way 451 Research (and other research firms) asked its question doesn’t reveal all the nuances that we see at Uptime Institute Intelligence and in fact their simpler questioning misses the fact that both total infrastructure capacity and the data center portion of it are both growing, albeit at different rates: Data Center based capacity is growing but at a slower rate than the total infrastructure capacity. Some big organizations are indeed shifting the bulk of their NEW work to the cloud, but they are simultaneously maintaining and even expanding a premium data center and some edge facilities. This is a complex topic to be sure.

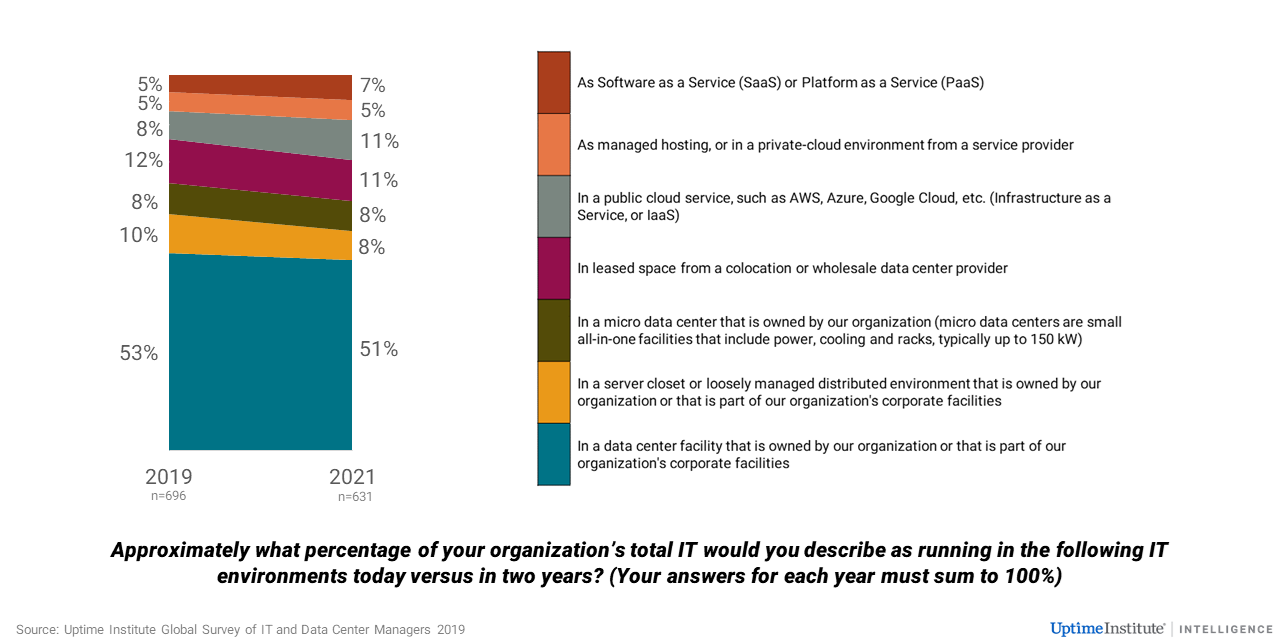

So let’s focus on brand new data gathered in 2019, with included much more granular questions, in the context of where capacity exists, and where business applications, old and new are being deployed. In Uptime Institute’s 2019 operator survey (which had results released in May 2019), Uptime Institute asked a more comprehensive question: “What percentage of your organization’s total IT would you describe as running in the following environments?” This question focused on percentage of existing workloads, rather than where the main workload was located or what would happen in the future (a more objective representation).

This Uptime Institute study confirmed that the shift to the public cloud and service oriented capacity was happening, but revealed that the shift was less dramatic and much slower than most industry reporters and pundits would suggest. Over 600 operators said that, in 2021, about half of all workloads will still be in enterprise data centers, and only 18% of workloads in public cloud/SaaS services. Just over three-quarters of all workloads, they believe, will still be managed by their own enterprise staff at a variety of locations that include enterprise data centers, co-location venues, server closets and micro/edge type data centers. The science of any survey confirms that the more granularity in the question, the more actionable the intelligence.

What are the takeaways from this? First, enterprise IT’s move to the cloud is real and strong, but it has not happened as dramatically, nor as fast as predicted, or in a way that is as binary, as many analysts and experts had reported. And for all the cloud oriented coverage published over the past dozen years which proclaimed the death of enterprise IT (and of the corporate data center itself), it is still quite premature. (Note: A considerable part of the public cloud workload reported elsewhere is actually comprised of consumer services, such as Netflix, Uber or Snapchat, which are not usually classed as enterprise IT.)

So what does it all mean? The IT ecosystem that already supports a diverse hybrid infrastructure is not yet facing a tipping point for any one portion. That doesn’t mean it won’t come eventually. Basic physics kicks in: workloads that are re-engineered to be cloud-compatible are much more easily moved to the cloud! But there are many other factors as well and as such, core infrastructure change will be gradual. These reasons including economics of work, dynamic scale-ability, risk management, support-ability, application support, overall performance, service reliability and the changing business models facing every modern business today. Simply put: The Enterprise IT environment is changing everyday and its hybrid nature is already very challenging, but Enterprise IT is not in eminent terminal decline.

Public cloud operators, meanwhile, will continue to assess what they need to do to attract more critical IT workloads. Uptime Institute Intelligence has found that issues of transparency, trust, governance and service need addressing — outstanding tools and raw infrastructure capacity alone are not sufficient. We continue to monitor the actual shifts in workload placements and will report regularly as needed.

More detailed information on this topic, along with a wealth of other strategic planning tools are available to members of the Uptime Institute Network, a members-only community of industry leaders which drive the data center industry. Detail can be found here.

2020

2020 Getty

Getty

2019, Getty

2019, Getty