Unravelling net zero

Many digital infrastructure operators have set themselves carbon-neutral or net-zero emissions goals: some large hyperscale operators claim net-zero emissions for their current operating year. Signatories to the Climate Neutral Data Center Pact, a European organization for owners and operators, aim to be using 100% clean energy by 2030.

All these proclamations appear laudable and seem to demonstrate strong progress for the industry in achieving environmental goals. But there is a hint of greenwashing in these commitments which raises some important questions: how well defined is “net zero”? What are the boundaries of the commitments? Are these time frames aggressive or the commitments meaningful?

There are good reasons for asking these questions. Analysis by Uptime Institute Intelligence suggests most operators will struggle to meet these commitments, given the projected availability of zero-carbon energy, equipment and materials and carbon offsets in the years and decades ahead. There are three core areas of concern that critics and regulators are likely to raise with operators: the use of renewable energy certificates (RECs), guarantees of origin (GOs) and carbon offsets; the boundaries of net-zero commitments; and the industry’s current lack of consensus on the time frame for attaining true net-zero operations.

RECs, GOs and carbon offsets

RECs and GOs are tradeable certificates representing 1 MWh of zero emissions of renewable energy generation; carbon offsets are certificates representing a quantity of carbon removed from the environment. All of these tools can be used to offset operational carbon emissions. Most current net-zero claims, and the achievement of near-term commitments (i.e., 2025 to 2035), depend on the application of these tools to offset the use of fossil-fuel-based energy.

Under currently accepted climate accounting methodologies, the use of RECs and offsets is a viable and acceptable way for digital infrastructure operators to help reduce emissions globally. However, using these certificates can distract from the real and difficult work of driving infrastructure efficiency improvements to increase the workload delivered per unit of energy consumed and the procurement of consumed clean energy to reduce the carbon emissions per unit of consumed energy toward zero.

Uptime Institute believes that stakeholders, regulators, and other parties will increasingly expect, and perhaps require, operators to focus on moving towards the consumption of 100% zero-emissions energy for all operations — that is, true net-zero emissions. This objective, against which net-zero claims will ultimately be judged, is not likely to be achieved in 2030 and perhaps not even by 2040: but it is an objective that deserves the industry’s full attention, and the application of the industry’s broad and varied technical expertise.

The boundaries of the net-zero commitment

Digital infrastructure operators have not adopted consistent accounting boundaries for their net zero commitments. While all operators include Scope 1 and 2 emissions, and while some do address Scope 3 emissions in full, others are ignoring these — completely or partially. There is no clear sector-wide consensus on this topic — either on which applicable Scope 3 emissions should be included in a goal, or in the classification or allocation of emissions in colocation facilities. This can create wide discrepancies in the breadth and scope of different operator’s commitments.

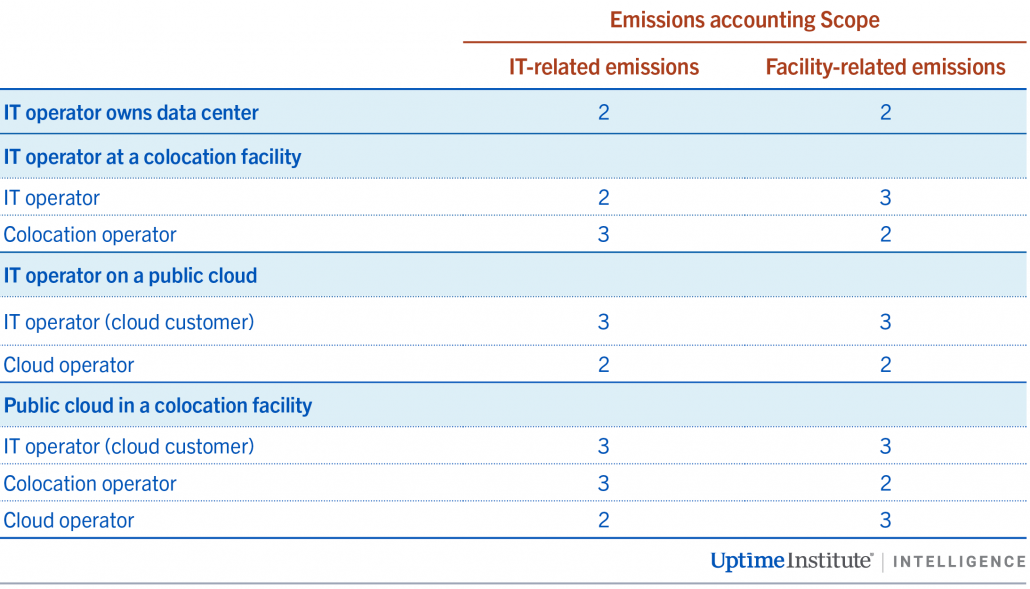

For most organizations running IT and / or digital infrastructure operations, the most consequential and important Scope 3 category is Category 1: Purchased goods and services — that is, the procurement and use of colocation and cloud services. The CO2 emissions associated with these services can be quantified with reasonable certainty and assigned to the proper scope category for each of the three parties involved in these services offerings — IT operators, cloud service operators and colocation providers (see Table 1).

Uptime Intelligence recommends that digital infrastructure operators set a net-zero goal that addresses all Scope 1, 2 and 3 emissions associated with their IT operations and / or facilities in directly owned, colocation and cloud data centers. IT operators will need to collaborate with their cloud and colocation service providers to collect the necessary data and set collaborative emissions-reductions goals. Service providers should be required to push towards 100% renewable energy consumption at their facilities. Colocation operators, in turn, will need to collaborate with their IT tenants to promote and record improvements in workload delivered per unit of energy consumed.

Addressing the other five Scope 3 categories applicable to the data center industry (embedded carbon in equipment and building material purchases; management of waste and end-of-life equipment; fuel and other energy-related activities; business travel; and employee commuting) — necessitates a lighter touch. Emissions quantifications for these categories typically have high degrees of uncertainty: and suppliers or employees are best positioned to drive their operations to net zero emissions.

Rather than trying to create numerical Scope 3 inventories and offsetting the emissions relating to these categories, Uptime Intelligence recommends that operators require their suppliers to maintain sustainability strategies and net-zero GHG emissions-reduction goals, and provide annual reports on progress in achieving these.

Operators, in turn, should set (and execute) consequences for those companies that fail to make committed progress — up to and including their removal from approved supplier lists. Such an approach means suppliers are made responsible for delivering meaningful emissions reductions, without data center operators duplicating either emissions-reduction efforts or offsets.

Insufficient consensus on the time frame for attaining true net-zero operations

There appears to be no industry-wide consensus on the time frame for attaining true net-zero operations. Many operators have declared near-term net-zero commitments (i.e., 2025 to 2035), but these depend on the use of RECs, GOs and carbon offsets.

Achieving a true net-zero operating portfolio by 2050 will require tremendous changes and innovations in both the data center equipment and energy markets over the next 28 years. The depth and breadth of the changes required makes it impossible to fully and accurately predict the timing and technical details of this essential transformation.

The transition to zero carbon will not be achieved with old or inefficient equipment. Investments will need to be made in more efficient IT equipment, software management tools, and in clean energy generation. Rather than buying certificates to offset emissions, operators need to invest in impactful technologies that increase data centers’ workload delivered per unit of energy consumed while reducing the carbon intensity of that energy to zero.

What does all this mean for net-zero commitments? Given the difficulties involved, Uptime Intelligence recommends that data center operators establish a real net-zero commitment for their IT operations that falls between 2040 and 2050 — with five- to eight-year sequential interim goals. Operators’ current goal periods should achieve emissions reductions based on current and emerging technologies and energy sources.

After the first goal period, each subsequent interim goal should incorporate all recent advances in technologies and energy generation — on which basis, operators will be able to reach further in achieving higher workloads and lower carbon emissions per unit of energy consumed. Suppliers in other Scope 3 categories, meanwhile, should be held responsible for achieving real net-zero emissions for their products and services.

The bottom line? Instead of relying on carbon accounting, the digital infrastructure industry needs to focus investment on the industry-wide deployment of more energy-efficient facilities and IT technologies, and on the direct use of clean energy.