Capital inflow boosts the data center market

Data centers are no longer a niche or exotic investment among mainstream institutional buyers, which are swarming to the sector. There is now a buyer for almost every type of data center — including traditional-infrastructure investors and sovereign wealth funds. How might this new mix of capital sources change the broader data center sector?

Traditional buyers will remain active

The number of data center acquisitions in 2019 will likely end up being a record high. Among the most active buyers, historically and to date, are data center companies, such as cloud, colocation and wholesale providers, as well as data center real estate investment trusts (REITs). They will continue to buy and sell, typically for strategic reasons — which means they tend to hold onto acquired assets.

Most are buying to expand their geographic footprint — not just to reach more customers, but also to be more appealing to large cloud providers, which are prized tenants because they attract additional customers and also tend to be long-term tenants. (Even if a cloud provider builds its own data center in a region, it will usually continue to lease space, provided costs are low, to avoid migration costs and challenges.) Facilities with rich fiber connectivity and/or in locations with high demand but limited space will be targets, including in Amsterdam, Frankfurt, Paris, northern Virginia and Singapore. Many will seek to expand in Asia, although to date there has been limited opportunity. They will also continue to sell off nonstrategic, third-tier assets or those in need of expensive refurbishment.

For many years, data center companies and REITs have competed with private equity firms for deals. Private equity companies have tended to snap up data centers, with a view toward selling them relatively quickly and at a profit. This has driven up the number of acquisition deals in the sector, and in some markets has driven up valuations.

More long-term capital sources move in

So, what is changing? More recently, firms such as traditional infrastructure investors and sovereign wealth funds have been acquiring data centers. Traditional infrastructure investors, which historically have focused on assets ranging from utility pipelines to transportation projects, have been the most active among new buyers.

The newcomers are similar in that they tend to have longer return periods (that is, longer investment timelines) and lower return thresholds than private equity investors. Many are buying data centers that can be leased, including wholesale for a single large cloud customer and colocation for multiple tenants.

Traditional infrastructure investors, in particular, will likely continue to take over data centers, which they now include as part of their definition of infrastructure. This means they view them as long-term assets that are needed regardless of macroeconomic changes and that provide a steady return. These investors include infrastructure funds, traditional (that is, non-data center) REITS and real estate investors.

In addition to being attracted to the sector’s high yields and long-term demand outlook, new investors are also simply responding to demand from enterprises looking to sell their data centers or to switch from owning to leasing. As discussed in the section “Pay-as-you-go model spreads to critical components” in our Trends 2020 report, the appetite of enterprises for public cloud, colo and third-party IT services continues to grow.

An influx of buyers is matching the needs of the sellers. As enterprises outsource more workloads, they need less capacity in their own data centers. Many are (or are in the process of) consolidating their owned footprints by closing smaller and/or regional data centers and moving mission-critical IT into centralized, often larger, facilities. Frequently, the data centers they’re exiting are in prime locations, such as cities, where demand for lease space is high, or in secondary regional markets that are under-served by colos. All types of investors are buying these enterprise data centers and converting them into multi-tenant operations.

Also common are sales with leaseback provisions (“leasebacks”), whereby an enterprise sells its data center and then leases it back from the new owner, either partially or wholly. This enables enterprises to maintain operational control over their IT but shed the long-term commitment and risk of ownership. This arrangement also affords flexibility, as the enterprise often only leases a portion of the data center. Small or regional colos are also seeking to sell their data centers, realizing that they lack the economies of scale to effectively compete with multi-national competitors.

More joint ventures

Another trend has been an increase in joint ventures (JVs), particularly by data center REITs, with these new types of investors. We expect more JVs will form, including with more infrastructure funds, to back more very large leased data centers for large cloud providers, which are struggling to expand fast and seek more leasing options (particularly build-to-suit facilities). At the same time, more enterprise data centers will be sold — increasingly to investors with long-term horizons — and converted into multi-tenant facilities.

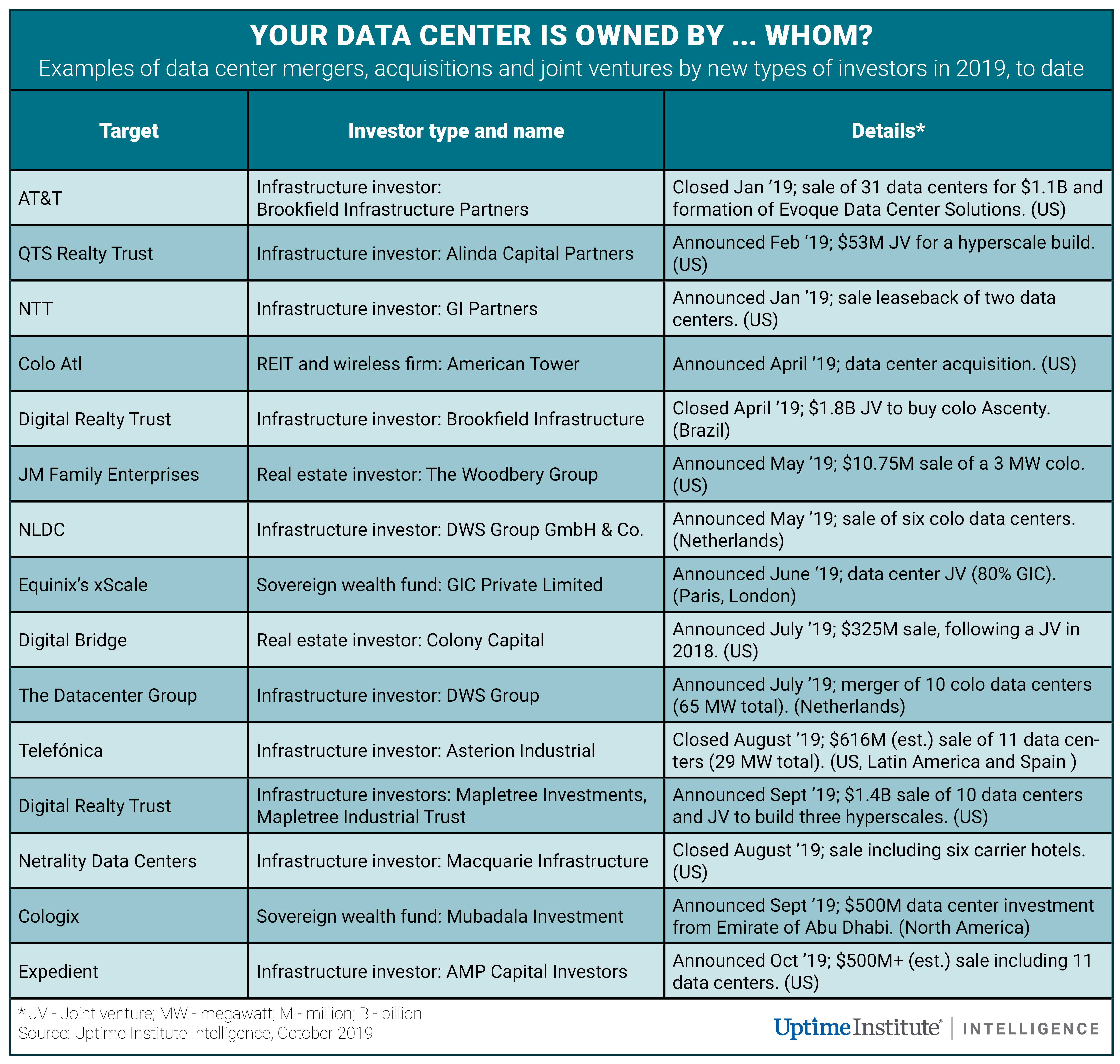

The table below highlights some of the non-traditional capital sources that acquired data centers in 2019.

As more of this type of long-term-horizon money enters the sector, the portion of facilities that are owned by short-term-horizon private equity investors will be diluted.

Overall, the new types of capital investors in data centers, with their deep pockets and long return timelines, could boost the sector. They are likely, for example, to make it easier for any enterprise wishing to give up data center ownership to do so.

The full report Ten data center industry trends in 2020 is available to readers here.

Getty

Getty

2020

2020

2019

2019

2019

2019 2019

2019